The Intangible Art of Operational Due Diligence

What do Greek statues have to do with the world of finance and investing? Brooks Ritchey, senior managing director, K2 Advisors®, Franklin Templeton Solutions®, takes a look at the heady topic of operational due diligence, using a cautionary tale of a well-known museum’s due diligence on one of its (perhaps not-so) ancient treasures to draw parallels to vetting alternative strategies or the managers of hedge strategies.

Brooks Ritchey

Brooks Ritchey

Brooks Ritchey

Senior Managing Director, K2 Advisors

Franklin Templeton Solutions

The following story is recounted by journalist Malcolm Gladwell in his book, Blink: The Power of Thinking Without Thinking (Little, Brown and Co., 2005).

The Statue That Wasn’t Right

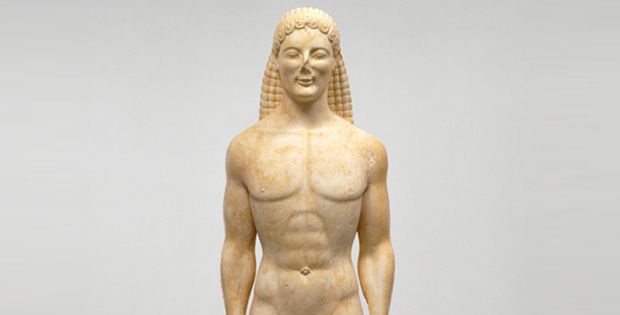

In September 1983, an art dealer approached the J. Paul Getty Museum in California with a marble statue he claimed dated from the sixth century B.C. The statue was what is known as a kouros, a free-standing ancient Greek sculpture representing a nude male figure. At that time there were only several hundred known kouroi in existence, and most of those were only broken fragments or partial busts. However, this one was unique in that it was in near-perfect condition. It stood nearly seven feet tall and was almost uniformly preserved. It was, if indeed a true kouros, an extraordinary treasure. The art dealer was asking the museum for US$10 million.

Naturally, the Getty sought to be thorough in its due diligence before committing to purchasing the statue. Was the sculpture consistent in look and design with other known authentic kouroi? Yes. Where was it found? The art dealer provided reams of documentation tracing its roots to a Greek archaeologist from the 1930s. Did the material it was made from appear authentic? Again, the answer was yes. A geologist from the University of California spent two days examining the surface of the statue with a high-resolution stereomicroscope.

A True Greek Kouros?

A True Greek Kouros?

He also removed a core sample and analyzed it using an electron microscope. It all checked out. The geologist determined the statue appeared to be made from dolomite marble from the ancient Cape Vathy quarry on the island of Thasos, and its surface was covered in a thin layer of calcite. The calcite was significant because the assumption was that dolomite could only turn to calcite over the course of hundreds, if not thousands, of years.

The Getty was satisfied with the investigation, and in their minds the kouros was indeed real. After a 14-month examination the museum agreed to buy the statue, and in the fall of 1986 it went on display as a special and rare antiquity. But was it?

Once available to the public, many expert art historians and aficionados excitedly went to view the kouros—and this is where the story gets interesting. Despite the Getty’s seemingly thorough investigation to establish authenticity, to the experts something about the kouros just did not feel right. Without any real tangible evidence to support their assessment, most just sensed the sculpture was somehow, off. The first one to point this out was an Italian curator, who found himself staring at the sculpture’s fingernails. In a way he could not immediately articulate, they just appeared wrong. Then a Greek expert expressed reservations. Then the director of the Metropolitan Museum of Art in New York described the kouros as “fresh looking,” not quite the adjective you would expect for a 2,000-year-old object. Months followed, and more experienced and veteran art historians visited the museum to see the statue. The chorus of skeptics grew louder. The Getty—with its army of geologists and lawyers and scientists, and having engaged in months and months of scrutiny—had come to the conclusion that the statue was real. Sculpture experts and art historians, however, after having only viewed the statue momentarily and from a distance, disagreed. Within the first few seconds of gazing upon it, Angelos Delivorrias, director of the Benaki Museum in Athens, described an “intuitive repulsion,” an innate sense that it was a fake.

Long story short, today the statue is widely considered by most to be bogus. As it turned out, a lot of the documents used to support its authenticity were forged. Also, as experts began to examine the statue in great detail, they realized that a hodgepodge of styles from many distinct time periods were reflected in it. Lastly, artificial means of creating the dolomitization observed on the statue’s surface have been demonstrated, thereby discounting the notion that the marble was centuries old. Of note, the Getty has never said definitively whether it believes the kouros is real or fake (certainly not after having paid $10 million!). Today the statue’s label reads “Greek, about 530 BC, or modern forgery.”

The Intangible Art of Operational Due Diligence

When discussing alternative investments or more specifically, hedge strategies and those who manage them, the importance of a quality operational due diligence (ODD) program cannot be overstated. In the view of most investment professionals, myself included, ODD is critical to any holistic alternative investment process. While, according to modern portfolio theory, investors should be compensated for taking on investment risk, they are not paid for incurring operational risk, and so it is imperative that any and all efforts be made to identify and avoid hedge strategy managers who may introduce meaningful operational risk to a portfolio. I do strongly agree that—quite intuitively—robust operational due diligence could add tremendous value to an investment program. The question then remains, how does one define “robust”?

Naturally, there are industry standard practices and protocols associated with any quality ODD system. Significant amounts of time, energy and resources are also required. But perhaps the most important aspect of any successful ODD framework, a trait that cannot be easily measured or quantified and one that is subjective and learned from years of experience and wisdom is intuition—or rapid cognition. This is the “intangible art” of due diligence; the part that is about those “thin-slicing” seconds when subconscious decisions are sometimes made. While intuition may be an abstract component of successful ODD, we believe it is no less critical—just ask the Getty museum.

Rapid Cognition

Gladwell explores this concept of intuitive decision making in his aforementioned book. His supposition is that past experiences often allow people to make informed decisions very rapidly (in the “blink” of an eye), based upon subconscious interpretations of previous cues and events, which he describes as rapid cognition.

When you meet someone for the first time, for example, or walk into a house you are thinking of buying, or enter a new restaurant, or read the first few sentences of a resume, your mind—unbeknownst to your conscious self and in a matter of seconds—has already jumped to a series of conclusions. Gladwell believes those instant decisions are really powerful, important and, often really good. Of note, Gladwell avoids the word intuition in his book, suggesting it describes emotional reactions or gut feelings, the thoughts and impressions that don’t seem entirely rational. He believes what goes on in those first moments is perfectly rational. It is thinking, he says—just the kind that moves a little faster and operates a little more mysteriously than the kind of deliberate, conscious decision making that we usually associate with “thinking.”

From my view, the theories Gladwell puts forth do seem to have merit, at least at first glance. At a minimum, it seems reasonable to suggest that the more experience and practical application one has in a particular field, whether it be ODD or vetting antiquities, the better he/she will be at their job, and in applying so called rapid-cognition. Naturally this would be of great value in assessing the less black/white questions associated with ODD. How does one weigh facts against gut instincts? What is the appropriate balance between the desire to do a deal and negative information? Is there pressure to make an investment? Has the manager been given a suitable amount of time to respond effectively? Is the manager patient and candid in their responses? Can the manager be trusted?

The point is it is not only about hours put in (though a great many are required at great expense), nor is it about the depth or rigor of the due diligence questionnaire (DDQ) or other checklist documents applied to the exercise. Often the true test of an effective due diligence program is in the art, or the experience, of the investigators doing the work.

ODD: Avoiding Myopia

In my mind, there is little question that a robust ODD practice begins and ultimately ends with the quality and depth of professional experience of the staff executing the process. It is also a fluid exercise, and one that requires “outside-the-box” thinking in many instances. Senior Managing Director Andrew Kandiew, who has more than 30 years of accounting and fund operational experience and heads K2’s Operational Due Diligence team, has spoken about the need to avoid myopic thinking when conducting reviews. In his words:

“Global economies and markets are dynamic and perpetually in flux. Individuals change over time, responding differently to evolving situations and incentives. Strategies change over time. Every organization and process has its own series of investment and operational risks. That is to say, no due diligence questionnaire or architecture can cover all such risks, much less produce a definitive yes-or-no answer to investment opportunities. This is where the value of an experienced ODD team can be demonstrated.”

In other words, establishing a checklist or road map for an effective operational due diligence program can only be expected to serve as a starting point, or rough framework, for effective ODD. As the nature of our business is fluid, organic and sufficiently complex, any suitable ODD process needs to be in a similar state of evolution, such that new circumstances are recognized and demands are met. A static guidebook cannot suffice.

due diligence – It’s the People

Of note, an important aspect of the cost structure of ODD relates to the pedigree and experience of the staff on hand. For many organizations, less seasoned and more junior staff may be responsible for aspects of the analysis, if not for the entire process. Clearly, this would lend itself to a lower overhead cost in terms of human resources, although the quality of the analysis could very well suffer. As the adage says, you get what you pay for. This speaks directly to the notion of the intangible value of ODD when conducted by a sufficiently seasoned and experienced team.

In summary, the “artistic” nature of operational due diligence is a human exercise, and one that cannot be readily quantified and cataloged. One often needs to judge individuals and organizations based on limited exposures, and must discipline themselves to examine and reexamine assumptions and conclusions. The importance and value of the abstract or intangible qualities of a solid ODD program—wisdom, experience and judgment—cannot be overstated. This is the “art” of due diligence, the part that is about those “intuitive” seconds.

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

To get insights from Franklin Templeton Investments delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_US and on LinkedIn.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Any returns generated from alternative investment strategies may not adequately compensate investors for the business and financial risks assumed and there is no assurance any such strategy will be successful.

Investment in these types of strategies is subject to those market risks common to entities investing in all types of securities, including market volatility.

Beyond Bulls & Bears – Perspective from Franklin Templeton Investments (U.S.) – At Beyond Bulls & Bears, our mission is not to bring you the latest hot stock tip or bit of Wall Street gossip. It’s to share the on-the-ground, long-term perspectives of investment professionals adept at navigating the increasingly complex world of global investing. Markets change. The fundamentals of good investing don’t.